In the dynamic symphony of economic endeavors, the Finance Industry of Bangladesh stands as a resilient crescendo. Amidst financial breakthroughs and diverse fiscal landscapes, this sector plays a vital role in shaping the economic harmony of the nation.

Bangladeshi Financial Industry Overview:

Monetary Policy Tools:

Non-Performing Loans (NPL) Situation:

Stock Market and Bond Market:

Taxation in Financial Industry:

Trends in Financial Inclusion and Digitalization:

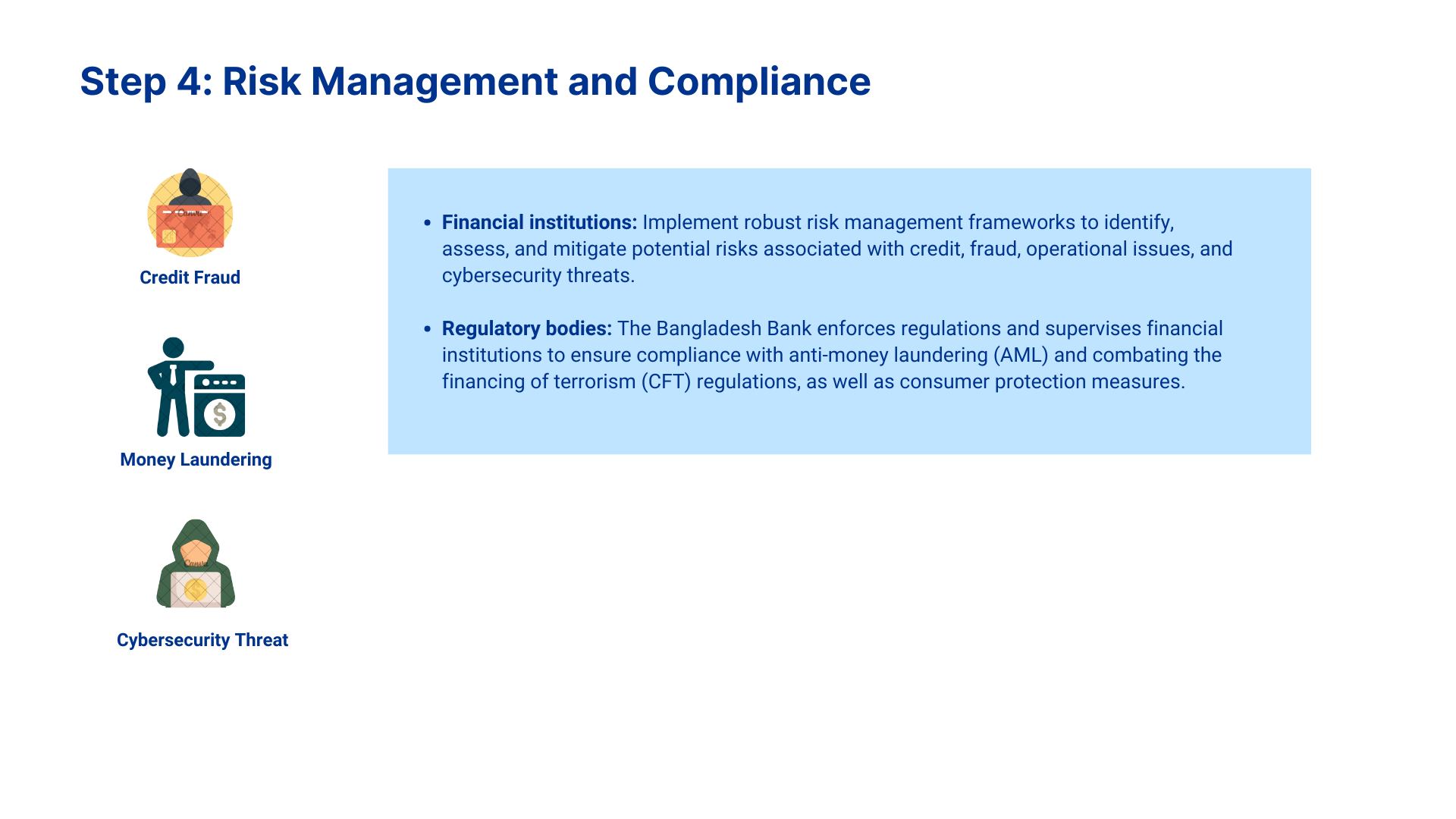

Challenges:

Organizations endowed with substantial financial resources actively participate in investment endeavors, strategically deploying their surplus funds into either debt instruments or equity instruments emanating from entities facing fiscal shortfalls. The choices available for these surplus entities include opting to deposit funds within financial institutions like banks or venturing into alternative investment avenues such as National Security Certificates and bonds.

In the realm of equity investments, surplus units have the option to engage in stock markets, entrust their funds to specialized entities like Asset Management Companies (AMCs), or explore promising opportunities within the dynamic landscape of startup ventures. This discerning allocation of surplus funds underscores a multifaceted and diversified approach to investment, thereby contributing significantly to the overall efficacy and vibrancy of financial markets. This strategic diversification not only enhances financial resilience but also fosters a robust and dynamic investment ecosystem.

The revenue of the financial sector majorly depends on:

1. Interest income: This remains the primary source of revenue for most banks and financial institutions, generated through (a) Loan interest: Interest charged on loans disbursed to individuals, businesses, and other entities. (b) Investments: Income earned from investments in government securities, corporate bonds, and other financial instruments.

2. Fee income: Fees charged for various services like: (a) Transaction fees: Account maintenance, cash withdrawals, money transfers, etc. (b) Service charges: Loan processing fees, underwriting fees, trade finance fees, etc. (c) Advisory fees: Investment advice, wealth management services, etc.

3. Foreign exchange: Income earned from buying and selling foreign currencies.

4. Islamic banking income: Profit-sharing models and fee-based structures specific to Islamic financial products.

5. Microfinance: Interest income and fees charged on small loans to low-income individuals and small businesses.

Major cost drivers of the financial sector are:

1. Interest expense: Cost of funds incurred by banks and financial institutions to maintain reserves and borrow money for lending.

2. Employee Benefits: Commissions, benefits, and training costs for staff across various functions.

3. Operational expenses: Rent, utilities, technology infrastructure, marketing, and other overhead costs.

4. Loan impairment charges: Provisions set aside to cover potential losses on non-performing loans.

5. Regulatory compliance costs: Costs associated with adhering to regulations and reporting requirements of Bangladesh Bank.

6. Technology investments: Upgrading and maintaining core banking systems, mobile banking platforms, and other digital infrastructure.

The Porter’s Five Forces analysis for the Financial industry in Bangladesh are outlined below. These factors impact how businesses compete and conduct business in Bangladesh's Financial sector, hence defining the sector's strategic landscape.

1. Threat of New Entrants (Moderate): Regulatory requirements, capital adequacy norms, and technological infrastructure pose moderate barriers. Established players have brand recognition and customer inertia, creating some switching costs. Government policies: New licenses and regulations can make entry challenging. FinTech and mobile banking pose potential competitive threats but also create opportunities for collaboration.

2. Bargaining Power of Suppliers (High): The suppliers here represent the surplus fund providers i.e., individual households and depositors. As this is a very highly regulated industry, the government catalyzes this high bargaining power of suppliers.

3. Bargaining Power of Buyers (High): Individuals, SMEs, corporations, and government entities present varied needs and bargaining power. Customers are highly price-sensitive, especially for basic services. Customers are becoming more aware of options and can switch between providers. Mobile wallets and microfinance institutions offer alternatives.

4. Threat of Substitutes (Moderate): Peer-to-peer lending platforms are emerging as alternatives for specific needs. Technology companies have started offering financial services like payments and digital wallets.

5. Competitive Rivalry (High): Numerous players across banking, NBFI, and MFIs, with varying competitive intensity in different segments. Overcrowding ignites Intense competition in retail banking and microfinance. Competition leads to lower prices and innovative offerings. Mergers and acquisitions are increasing, potentially reducing competition.

Future technical developments and government initiatives have the potential to greatly increase financial inclusion and attract more people into the formal financial system. Fintech solutions like online payments, e-wallets, and mobile banking are becoming more and more popular, which is predicted to promote financial efficiency and innovation even more. Bangladesh is a global leader in Islamic finance, and demand from both domestic and foreign markets is expected to drive the industry's continued expansion. Small and medium-sized businesses' (SMEs') access to financing is becoming more widely acknowledged as being essential to economic growth, which has led to the launch of new goods and services catered to this important market. Effectively controlling inflation, however, remains a constant challenge that could have an impact on interest rates, currency rates, and the stability of the financial system as a whole. Sturdy cybersecurity measures are essential to prevent financial fraud and data breaches as the reliance on digital platforms increases. Last but not least, preserving a sound and competitive financial climate requires walking the tightrope between encouraging innovation and guaranteeing responsible regulation.

Contact us today to schedule a free demo of FLOW - your all-in-one business management tool.